Cannacurio #119: Store Licensing Recap Q3 2025

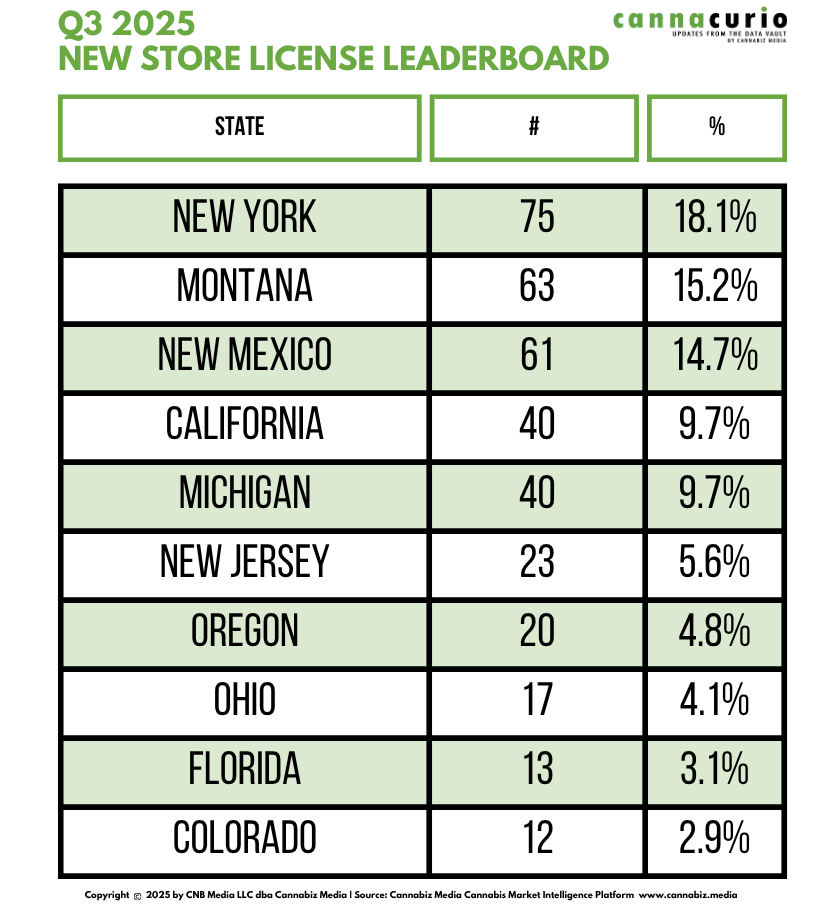

Newly licensed stores continue to make headlines as regulators and MSO’s tout these openings. Since they are the primary customer facing license along with delivery and consumption lounges, it is no wonder their comings and goings are chronicled. The 3rd quarter had 24 states issued 414 new licenses across the country. New York laid claim to 18% of those new “doors”.

Dispensary/Retail Key Point

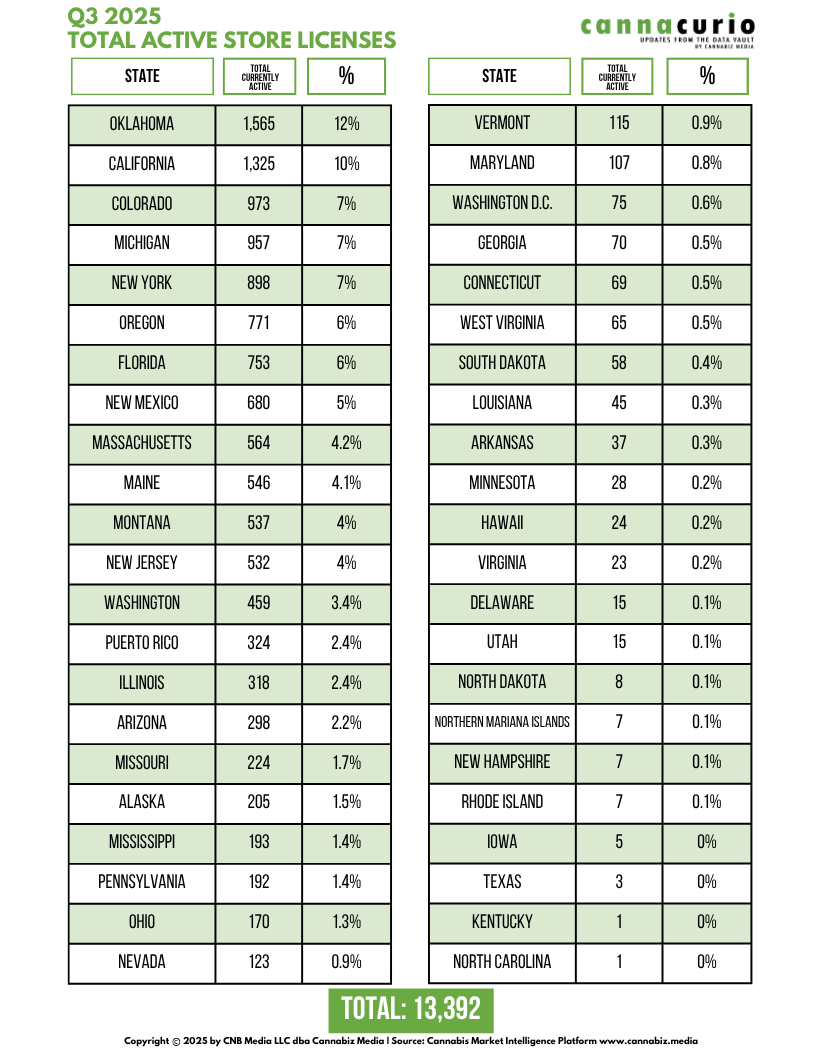

- There are 13,392 active store licenses, flat from 13,198 at the end of Q2

- 24 states added stores in Q3 down from 28 in Q2

- 414 new store licenses were issued in Q3 down from 420 in Q2

- Dutchie and Jane run the tech stack for most of the newly licensed stores

Cannabis Retail Market Trends – Q3 2025

The licensed cannabis retail market continues to face headwinds and opportunities—from regulatory flux, changing consumer expectations, price pressure, and substitution threats. Below are key themes that gained traction in Q3 2025.

1. Regulatory tug‑of‑war intensifies around hemp‑derived THC and federal classification

The United States House of Representatives appropriations subcommittee advanced a bill in July that would bar theDepartment of Justice from using federal funds to re‑schedule cannabis fromSchedule I, signaling political resistance to major federal reform. Meanwhile, the United States Senate Appropriations Committee approved a bipartisan proposal to redefine hemp and ban upwards of 90 % of hemp‑derivedTHC products (including THCA flower and delta‑8/10), which would further restrict the substitute market.

2. Market maturation and price compression in established adult‑use states

In mature markets such as California andIllinois, the industry is experiencing oversupply, price competition, and job losses. In a Q3 2025 update from Vangst and Whitney Economics, the industry reported about 15,000 jobs lost(‑3.4 %) due to price compression and saturation.

3. Substitution risk from hemp and outside channels remains—but is tilting

While the hemp‑derived THC space has been a major competitive threat, the impending federal and state regulatory crackdowns suggest the “loophole” channel may shrink — reducing one substitute threat. That said, consumers still have alternatives (illicit, hemp‑derived, alcohol)so licensed stores must maintain value and differentiation to retain share.

4. Licensing growth concentrated

Licensed store growth is moving faster in select states like New York, New Mexico, Montana, California and Michigan. For retail operators, this means geographic opportunity exists—but this growth may also bring competition and price pressure as more stores enter.

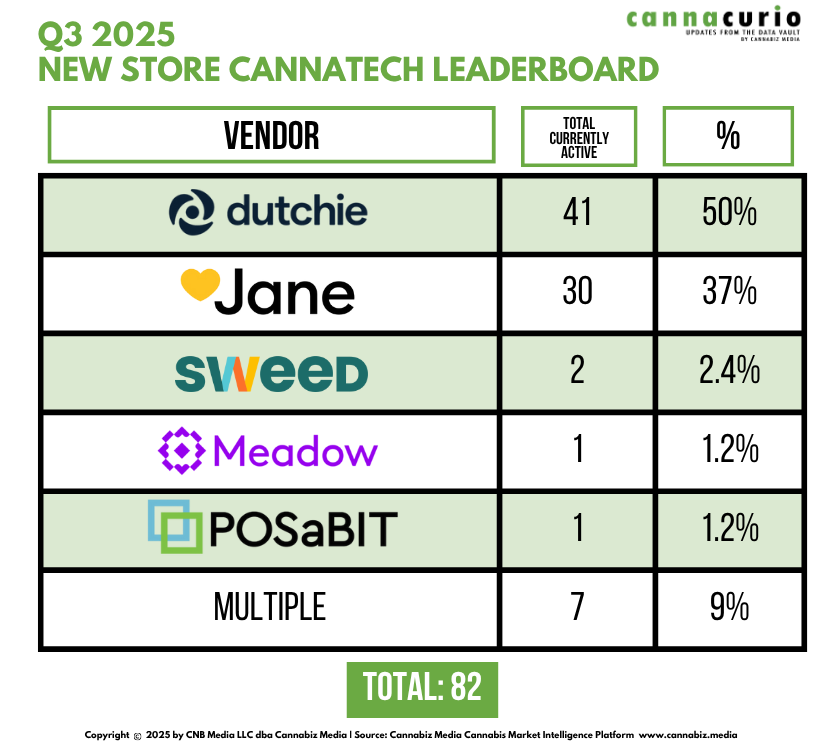

Tech Stack

Emerald Intel researches the tech stack of Active US cannabis stores. We wanted to get a sense of which vendors are making strides in the 414 newly active stores from last quarter. Two vendors own that leaderboard: dutchie and Jane combined for 87% of the market share. Although we only found data for 20% of those newly active stores, these two vendors obviously have a strong go-to-market strategy:

Dispensary/Retail

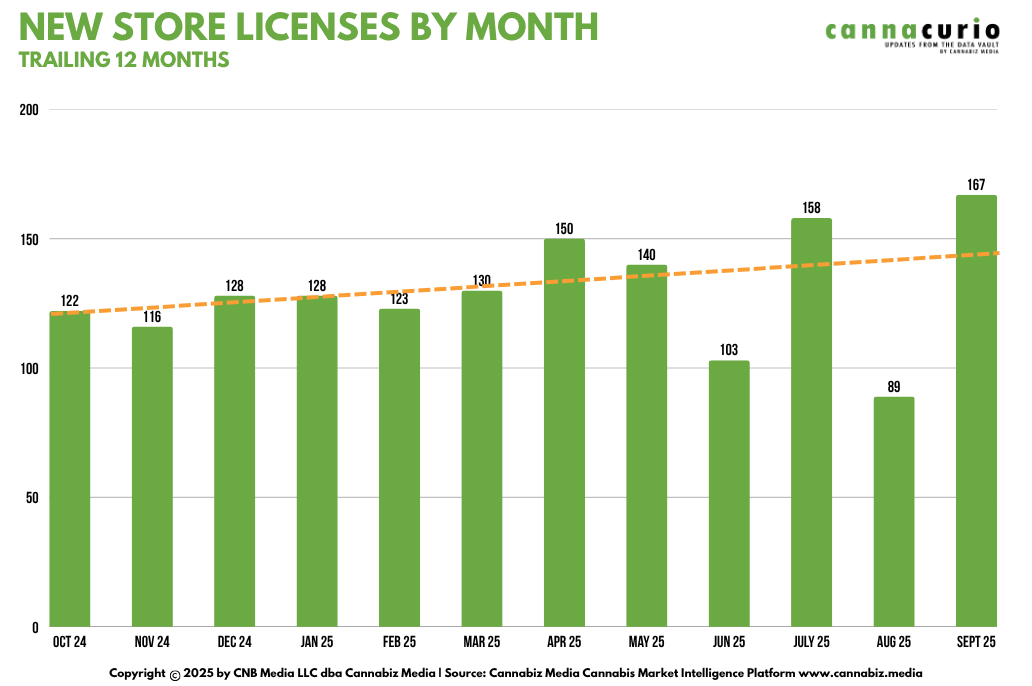

Store openings still generate news and press releases. As the primary customer-touching license, they generate the most interest. They also face stiff competition from the illicit market as well as smoke, vape and CBD shops in some states. The graph below and trend line show a gentle upswing in new licenses nationwide.

In the Store Leaderboard, New York has held onto their leadership position since Q4 2024; and accounted for almost twenty percent of all new store licenses issued in Q3 nationwide.

The following table highlights the total census of cannabis retailers by state. Oklahoma still leads the nation even with all the licenses that have shuttered, and the ongoing moratorium.

Conclusion

Despite market headwinds, consolidation, and competition from hemp and illicit channels, the number of licensed stores continues to inch upward—demonstrating the resilience of the cannabis retail sector. Growth remains concentrated in markets like New York, California, and Michigan while mature states work through price and saturation pressures. One upcoming jurisdiction to monitor is Virginia, where a newly elected Democratic governor may finally advance the state’s long-delayed retail cannabis program—potentially adding another major market to the national map.

Author

Ed Keating is a co-founder of Cannabiz Media and oversees the company’s data research and government relations efforts. He has spent his career working with and advising information companies in the compliance space. Ed has managed product, marketing, and sales while overseeing complex multi jurisdictional product lines in the securities, corporate, UCC, safety, environmental, and human resource markets.

AtCannabiz Media, Ed enjoys the challenge of working with regulators across the globe as he and his team gather corporate, financial, and license information to track the people, products, and businesses in the cannabis economy.

Ed graduated from Hamilton College and received his MBA from the Kellogg School at Northwestern University.

Cannabiz Media customers can stay up-to-date on these and other new licenses through our newsletters, alerts, and reports modules. Subscribe to our newsletter to receive these weekly reports delivered to your inbox. Or you can schedule a demo for more information on how to access the Cannabiz Media Cannabis Market Intelligence Platform yourself to dive further into this data.

Cannacurio is a regular column from Cannabiz Media featuring insights from the most comprehensive license data platform. Catch up on Cannacurio posts and podcasts for the latest updates and intel.

Need more insights?

.png)